Statistical Inference#

So far, we have seen methods for describing a sample of data (descriptive statistics) and we have reasoned on abstract concepts using basic probability theory concepts. In practice, we are often interested in the properties of a population, rather than a sample or some abstract quantities. Examples are:

What is the percentage of votes each candidate will get at an election?

What is the proportion of defective goods in a manufacturing process?

Is there a relationship between smoking and developing a given disease in the world population?

One approach to answer these questions would be to collect the whole population, but this is often unfeasible (e.g., interviewing all voters) and sometimes impossible.

The statistician’s approach is instead to sample a subset of the whole population and try to infer some of the properties of the population from the sample. This part of statistics is called statistical inference. Analyzing data using such techniques is often called an inferential analysis. In this part of the course, we will review different statistical tools for inferential analysis and show some concrete examples, without giving a formal definition of such tools, which is left to other courses.

Sampling#

The first step towards an inferential analysis is the sampling process. When we acquire a pre-made dataset, sampling is already done, while when we collect data, we are actually sampling from the population. In both cases, it is important to reason on the properties of the sample we will work on.

Simple random sample#

The easiest way to sample from a population is randomly. A simple random sample makes two assumptions:

Unbiasedness: each element of the population has the same probability of being selected;

Independence: selecting one of the elements of the population does not affect the selection of the other elements in any way.

This approach guarantees that, if we collect a large number of elements, the obtained sample will be a good representative of the population. For instance, if in the population of interest we have \(10\%\) of people over \(70\), we expect this proportion to be roughly represented in the sample as well.

An example of bad sampling:

We want to ask the inhabitants of a city whether they are satisfied with the quality of life in that city. To sample a large quantity of subjects, we go to the main square and ask passengers to reply to a few questions. If a ground of friends stops we interview all of them to maximize the number of examples we can obtain.

The sampling design outlined above has two important issues:

Unbiasedness: the selection process is biased (selection bias). We selected a single location in the city (the main square) and hence we are oversampling people who tend to spend time there (e.g., because they work in the city center), versus people who do not spend much time there (e.g., because they work in the periphery).

Independence: when we interview groups of people, in fact, we are breaking the independence assumption, Indeed, selecting one of the people is not independent of selecting others (the members of the same group).

Another example of flawed sampling:

We want to check how many people believe a given conspiracy theory. To do so, I send a message to all my contacts (\(500\)). About \(200\) of them reply to my message and \(180\) of them say they do believe that theory. \(80\%\) of people actually believe it!

Also here there are important issues:

Selection bias: I am not randomly sampling. Instead, I am choosing among my contacts.

Response bias: Only \(200\) people replied. Chances are that only people who are very motivated will reply. Maybe most of the believers did, while the others just ignored my message.

Another example:

We interview people on their voting preferences by dialing random phone numbers.

While this may seem sound, we will not end up with a simple random sample because we will not select people without a phone number and we will oversample people with more than one numbers (e.g., work and home).

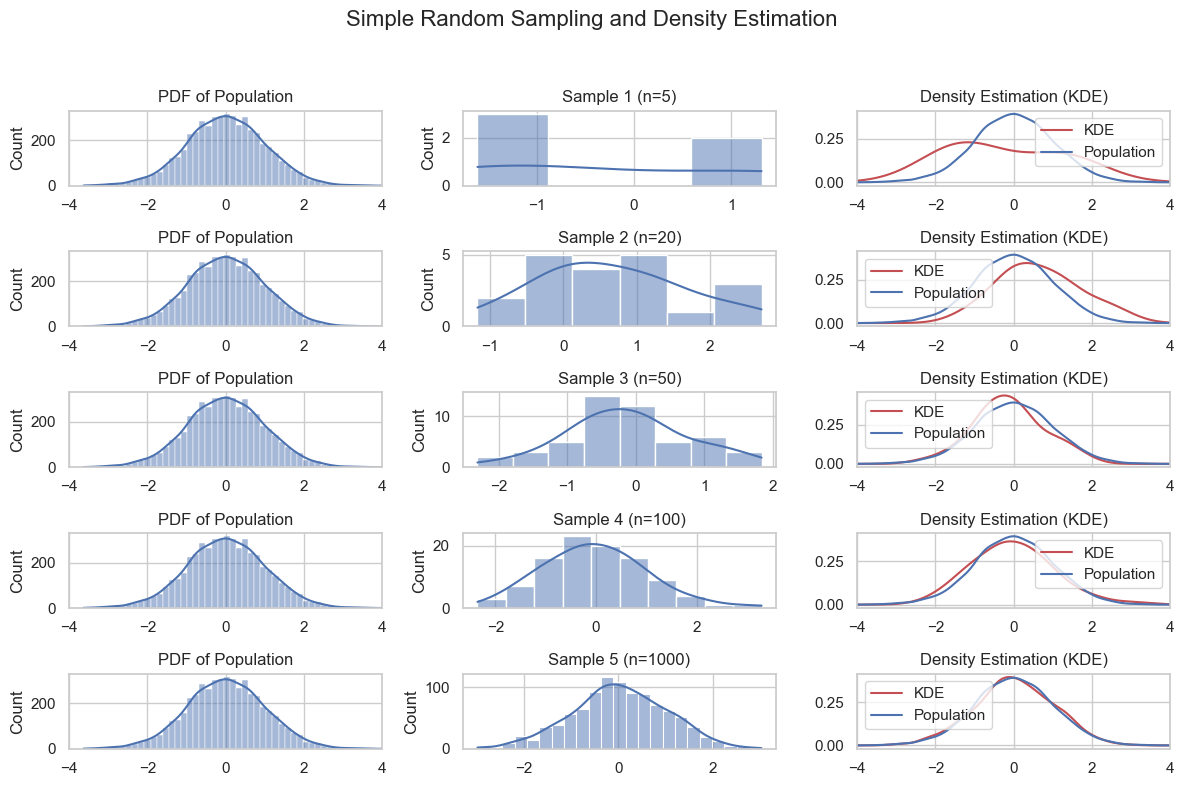

The plot below shows the importance of sample size:

Stratified Sampling#

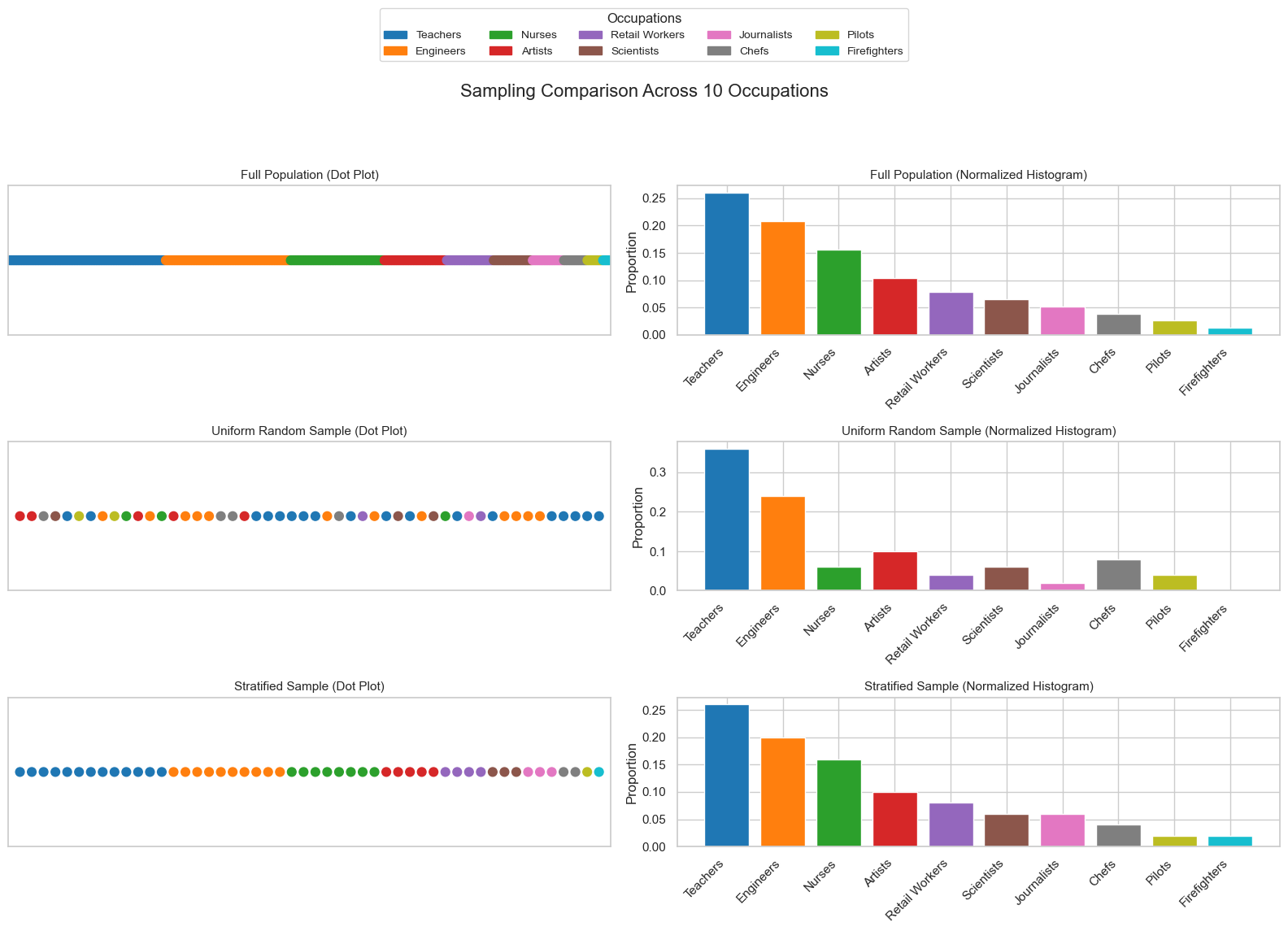

Sometimes, the population under study is heterogeneous, meaning it contains distinct subgroups with different characteristics. In such cases, simple random sampling may fail to capture the diversity of the population, leading to under-representation of certain groups.

For example, suppose we hypothesize that the variable Occupation influences voting preferences. If we randomly sample from the entire population, we might unintentionally select too few individuals from certain occupations, skewing our results.

To address this, we can use stratified sampling. This involves:

Dividing the population into homogeneous subgroups (strata) based on a relevant variable, such as

OccupationPerforming random sampling within each stratum, ensuring proportional representation

This method improves representativeness but requires prior knowledge or assumptions about the population structure.

The figure below shows a heterogeneous population, a sample obtained via uniform random sampling, and a sample obtained via stratified sampling.

Sampling in Python#

In Python we can easily sample from known distributions using numpy random module, as shown in the example below:

import numpy as np

import matplotlib.pyplot as plt

# Set the sample size

sample_size = 1000

# Sample from the Normal (Gaussian) Distribution

mean_normal = 0

std_dev_normal = 1

samples_normal = np.random.normal(mean_normal, std_dev_normal, sample_size)

# Sample from the Exponential Distribution

rate_exponential = 0.5

samples_exponential = np.random.exponential(1/rate_exponential, sample_size)

# Sample from the Uniform Distribution

low_uniform = 0

high_uniform = 1

samples_uniform = np.random.uniform(low_uniform, high_uniform, sample_size)

# Sample from the Laplace Distribution

loc_laplace = 0

scale_laplace = 1

samples_laplace = np.random.laplace(loc_laplace, scale_laplace, sample_size)

# Sample from the Poisson Distribution

lam_poisson = 3

samples_poisson = np.random.poisson(lam_poisson, sample_size)

# Create histograms to visualize the distributions

plt.figure(figsize=(15, 3))

plt.subplot(1, 5, 1)

plt.hist(samples_normal, bins=30, color='blue', alpha=0.7)

plt.title('Normal Distribution')

plt.subplot(1, 5, 2)

plt.hist(samples_exponential, bins=30, color='green', alpha=0.7)

plt.title('Exponential Distribution')

plt.subplot(1, 5, 3)

plt.hist(samples_uniform, bins=30, color='red', alpha=0.7)

plt.title('Uniform Distribution')

plt.subplot(1, 5, 4)

plt.hist(samples_laplace, bins=30, color='purple', alpha=0.7)

plt.title('Laplace Distribution')

plt.subplot(1, 5, 5)

plt.hist(samples_poisson, bins=30, color='orange', alpha=0.7)

plt.title('Poisson Distribution')

plt.tight_layout()

plt.show()

We can also sample from an existing sample to obtain a subsample. This can be done starting from a dataset. For instance, let us consider the weight-height dataset:

import pandas as pd

data=pd.read_csv('http://antoninofurnari.it/downloads/height_weight.csv')

data.info()

data.head()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 4231 entries, 0 to 4230

Data columns (total 4 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 sex 4231 non-null object

1 BMI 4231 non-null float64

2 height 4231 non-null float64

3 weight 4231 non-null float64

dtypes: float64(3), object(1)

memory usage: 132.3+ KB

| sex | BMI | height | weight | |

|---|---|---|---|---|

| 0 | M | 33.36 | 187.96 | 117.933920 |

| 1 | M | 26.54 | 177.80 | 83.914520 |

| 2 | F | 32.13 | 154.94 | 77.110640 |

| 3 | M | 26.62 | 172.72 | 79.378600 |

| 4 | F | 27.13 | 167.64 | 76.203456 |

We can obtain a subsample of 1000 observations as follows:

sample1=data.sample(1000)

sample1.info()

sample1.head()

<class 'pandas.core.frame.DataFrame'>

Index: 1000 entries, 129 to 3443

Data columns (total 4 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 sex 1000 non-null object

1 BMI 1000 non-null float64

2 height 1000 non-null float64

3 weight 1000 non-null float64

dtypes: float64(3), object(1)

memory usage: 39.1+ KB

| sex | BMI | height | weight | |

|---|---|---|---|---|

| 129 | M | 33.90 | 182.88 | 113.398000 |

| 3065 | F | 22.32 | 162.56 | 58.966960 |

| 2755 | M | 31.68 | 185.42 | 108.862080 |

| 3505 | F | 21.65 | 165.10 | 58.966960 |

| 1785 | F | 20.92 | 162.56 | 55.338224 |

Sampling will be random and uniform. As can be seen the indexes of the rows are shuffled. By default, Pandas will sample without replacement. We can sample with replacement specifying replace=True. For instance, we can obtain a larger sample (with repetitions) as follows:

sample2=data.sample(5000, replace=True)

sample2.info()

sample2.head()

<class 'pandas.core.frame.DataFrame'>

Index: 5000 entries, 1637 to 1037

Data columns (total 4 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 sex 5000 non-null object

1 BMI 5000 non-null float64

2 height 5000 non-null float64

3 weight 5000 non-null float64

dtypes: float64(3), object(1)

memory usage: 195.3+ KB

| sex | BMI | height | weight | |

|---|---|---|---|---|

| 1637 | F | 26.53 | 157.48 | 65.77084 |

| 4082 | M | 26.54 | 177.80 | 83.91452 |

| 1890 | F | 28.33 | 152.40 | 65.77084 |

| 3205 | M | 24.39 | 177.80 | 77.11064 |

| 477 | F | 24.02 | 162.56 | 63.50288 |

We can perform stratified sampling as follows:

# Define the stratification variable

strata_variable = 'sex'

# Number of samples per stratum

samples_per_stratum = 500

# Perform stratified sampling with include_groups=False

stratified_sample = (

data.groupby(strata_variable, group_keys=False)

.apply(lambda x: x.sample(samples_per_stratum), include_groups=True)

.reset_index(drop=True)

)

# Inspect the result

stratified_sample.info()

stratified_sample.head()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 1000 entries, 0 to 999

Data columns (total 4 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 sex 1000 non-null object

1 BMI 1000 non-null float64

2 height 1000 non-null float64

3 weight 1000 non-null float64

dtypes: float64(3), object(1)

memory usage: 31.4+ KB

/var/folders/cs/p62_d78d49n3ddj0xlfh1h7r0000gn/T/ipykernel_62824/1972380443.py:10: DeprecationWarning: DataFrameGroupBy.apply operated on the grouping columns. This behavior is deprecated, and in a future version of pandas the grouping columns will be excluded from the operation. Either pass `include_groups=False` to exclude the groupings or explicitly select the grouping columns after groupby to silence this warning.

.apply(lambda x: x.sample(samples_per_stratum), include_groups=True)

| sex | BMI | height | weight | |

|---|---|---|---|---|

| 0 | F | 26.31 | 170.18 | 76.203456 |

| 1 | F | 27.45 | 167.64 | 77.110640 |

| 2 | F | 28.29 | 165.10 | 77.110640 |

| 3 | F | 30.03 | 162.56 | 79.378600 |

| 4 | F | 29.16 | 162.56 | 77.110640 |

Note that, with this method, sampled observations will be sorted by sex. To get rid of this bias, we can shuffle the dataframe as follows:

stratified_sample = stratified_sample.iloc[np.random.choice(len(stratified_sample), len(stratified_sample), replace=False)]

stratified_sample.head()

| sex | BMI | height | weight | |

|---|---|---|---|---|

| 898 | M | 26.55 | 175.26 | 81.646560 |

| 452 | F | 29.01 | 162.56 | 76.657048 |

| 665 | M | 28.89 | 187.96 | 102.058200 |

| 200 | F | 31.26 | 152.40 | 72.574720 |

| 378 | F | 21.92 | 170.18 | 63.502880 |

Males and females will be perfectly balanced by design in this stratified sample:

stratified_sample['sex'].value_counts()

sex

M 500

F 500

Name: count, dtype: int64

Sampling Distribution of the Mean#

Let’s consider this problem:

A bakery sells packages of cookies labeled as weighing 1kg. Due to small variations in the production process, the actual weight of each package may differ slightly. To ensure quality, the bakery wants to verify that the average weight is close to the target.

We take a random sample of \(n = 1000\) packages and measure their weights \(x_1, x_2, \ldots, x_n\). We compute the sample mean:

This value is close to the target of 1000g, so we might conclude that the production process is accurate. But what if we took another sample? Would we get the same result?

This is still close to the target, but slightly lower than before. If we repeated this process many times, we would get a distribution of sample means.

We treat each package’s weight as a random variable \(X_i\), with:

where \(\mu\) and \(\sigma\) are the true mean and standard deviation of the population.

The sample mean \(\overline{X}\) is also a random variable:

Note that, while we cannot make assumptions for the individual \(X_i\), for the central limit theorem, we know that:

For large \(n\), the distribution of \(\overline{X}\) will be approximately normal, regardless of the shape of the original data.

We can derive the expected value, variance and standard deviation of \(X\) as follows:

We note that:

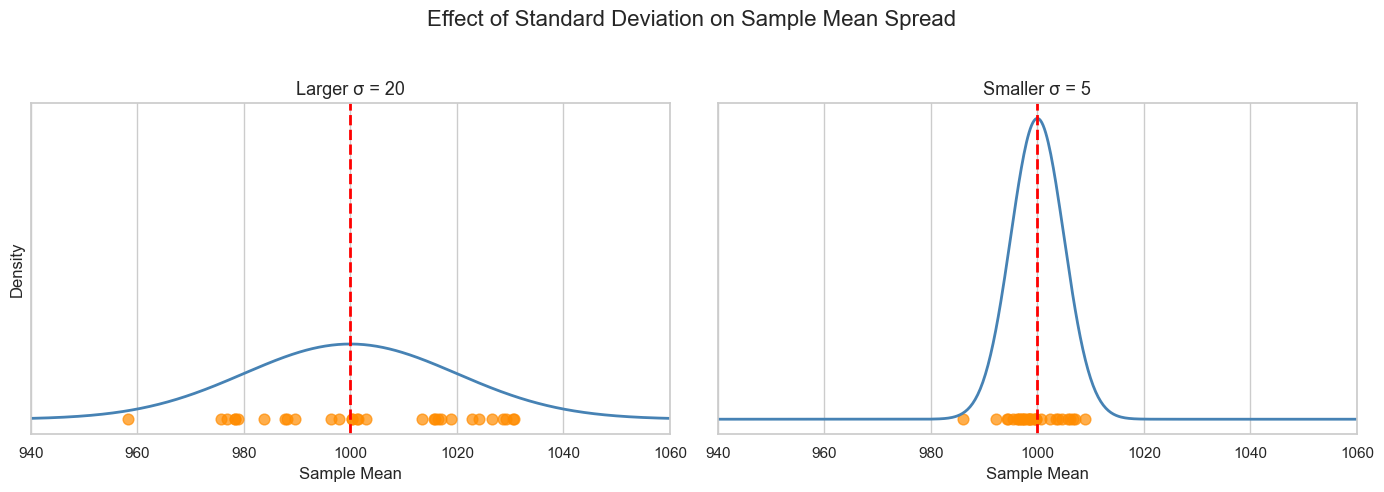

The expected value of the sample means (the mean of the means) converges to the mean of the population. This is the value we want to estimate: the actual average weight of packages.

The standard deviation of the distribution quantifies the precision according to which we can measure the mean. A small standard deviation indicates that sample means have small variability, so a single estimate will likely be closer to the true mean and hence more reliable.

This is exemplified by the following figure:

Standard Error#

While useful to quantify our precision in the estimation of the true mean, the standard deviation depends on the variance of the population, which is unknown.

In practice, we estimate it using the sample standard deviation:

and define the Standard Error (SE) as follows:

Similar to the standard deviation, the standard error quantifies our uncertainty in the estimation of the true mean.

Note that the standard error is inversely proportional to the square root of the sample size:

This relationship is common in many statistical estimators. It means that:

If we double the sample size, the error reduces by about 30%.

To halve the error, we need to quadruple the sample size.

This is a key insight: reducing uncertainty requires much more data than we might expect.

The standard error tells us how close our sample mean \(\overline{x}\) is likely to be to the true mean \(\mu\). A small standard error means that repeated samples will yield similar results, and our estimate is precise. A large standard error means more variability and less confidence in the estimate.

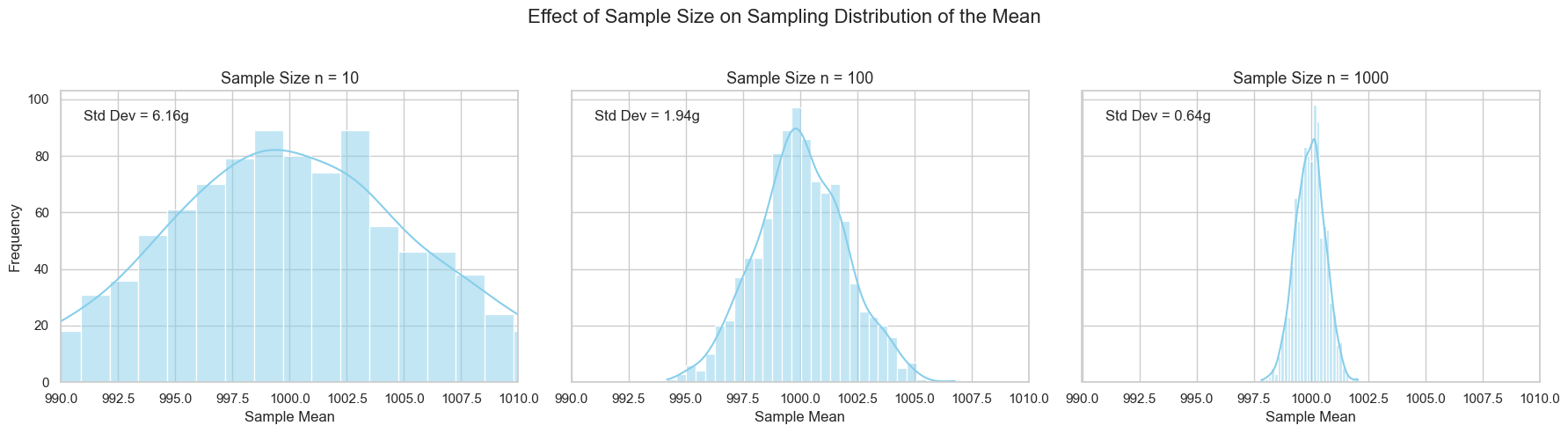

This is shown in the graph below:

This figure illustrates how sample size affects the precision of the sample mean. Each panel shows the distribution of sample means obtained by repeatedly sampling from the same population (mean = 1000g, standard deviation = 20g), but with different sample sizes:

Left (n = 10): The distribution is wide, indicating high variability. Small samples lead to more fluctuation in the estimated mean.

Center (n = 100): The distribution narrows, showing improved stability. The sample means are more tightly clustered around the true mean.

Right (n = 1000): The distribution is very narrow. Large samples yield highly consistent estimates, with minimal deviation from the true mean.

This visual reinforces the key idea that larger samples reduce the standard error, making our estimates more reliable. The spread of the sampling distribution shrinks proportionally to \(1/\sqrt{n}\).

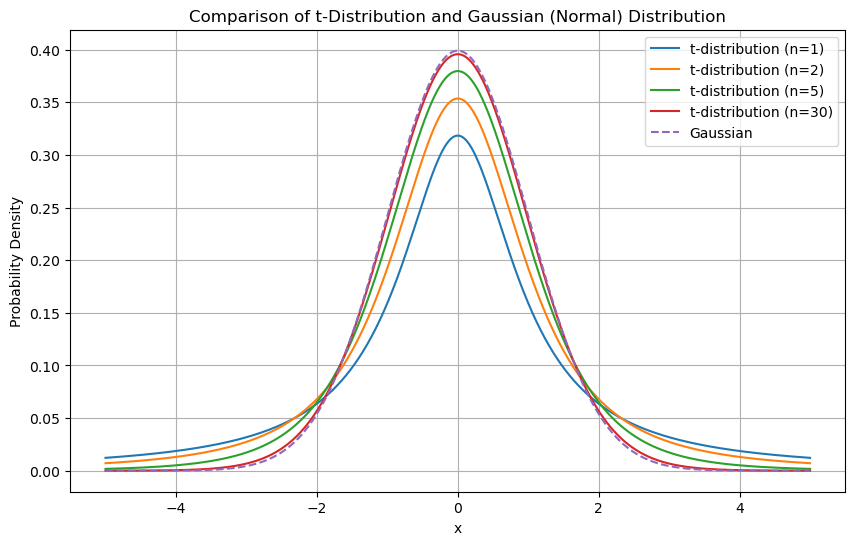

t-Student Distribution#

When \(n\) is small, the distribution of \(\overline{X}\) is not exactly normal. Instead, we use the t-Student distribution, which accounts for extra uncertainty:

This follows a t-distribution with \(n - 1\) degrees of freedom. The t-distribution looks like a Gaussian but has heavier tails, meaning more room for extreme values. As \(n\) increases, the t-distribution converges to the normal distribution.

Note that the t-Student distribution is obtained by applying standardization using the standard error rather than the standard deviation (which is unknown).

The relationship between a t-Student and Gaussian distribution is shown in the figure below:

As \(n\) gets larger, the t-Distribution approximates a Gaussian distribution.

We can now characterize how the means will distribute. In particular, for large values of \(n\), sample means will distribute according to a Gaussian distribution with standard deviation equal to the sample standard deviation.

Confidence Intervals#

Let’s return to our bakery example. We want to estimate the true average weight \(\mu\) of cookie packages, which are labeled as 1kg. We take a sample of \(n = 1000\) packages and compute:

This is our estimate of the true mean. However, we know that this value may vary depending on the sample we draw. If we took another sample, we might get a slightly different result. It is interesting to define the bounds of such variation, to understand where the true mean \(\mu\) is likely to be found relative to our estimate \(\overline{x}\).

Remember that the sample mean \(\overline{X}\) follows a Gaussian distribution centered at \(\mu\) due to the Central Limit Theorem.

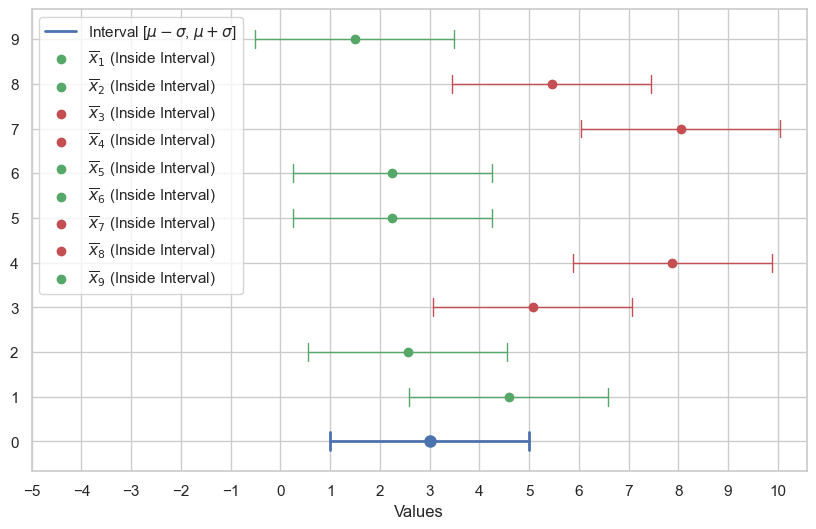

We also know that about \(68.3\%\) of the density of the Gaussian distribution will be within \(\mu-\sigma\) and \(\overline{x}+\sigma\), so we can write:

Which means that, if we perform several independent samplings, with sample size \(n\), the probability of obtaining a defect rate \(\overline{x}\) in the range \([\mu-\sigma, \mu+\sigma]\) is \(68.3\%\).

It is easy to show that:

This is graphically shown in the plot below. The blue segment is the one of bounds \([\mu-\sigma, \mu+\sigma]\). Note that, all times a point \(\overline{x}\) happens to be in the blue segment centered around \(\mu\), then \(\mu\) is in the segment centered around \(\overline{x}\).

This allows us to write:

which has a powerful interpretation:

If we draw many independent samples of size \(n\) and compute \(\overline{x}\) from the samples, the true mean \(\mu\) will lie in the interval \([\overline{x}-\sigma, \overline{x}+\sigma]\) \(68.3\%\) of the times

Alternatively

We can say with a confidence of \(68.3\%\) that the true mean will be in the \([\overline{x}-\sigma, \overline{x}+\sigma]\) interval.

In this context, \([\overline{x}-\sigma, \overline{x}+\sigma]\) is called a confidence interval.

We still have to compute actual numbers for our confidence interval, but we don’t have the standard deviation \(\sigma\). In practice, we replace it with the standard error and obtain the confidence interval:

We note that \(68.3\) is a very peculiar number and also a relatively low probability. In general, given a chosen percentage \(p\), that we call a confidence level, we can obtain a number \(\beta\) such that:

leading to the following confidence interval:

Alternatively, we will say that we chose a significance level \(\alpha=0.05\), which quantifies the number of times we admin the true mean will be out of the confidence interval.

It is very common to set \(\alpha=0.05\), which leads to \(\beta=1.96\) and the following confidence interval:

Computing Confidence Intervals in Practice#

We have seen how to compute confidence interval “by hand” in the case of the estimation of proportions (defect rate).In practice, depending on the quantities for which we want to estimate confidence bounds, we will need to use different distributions. For instance, when estimating means, we will have to use the t-Student distribution with \(n-1\) degrees of freedom. We will not see all methods in detail, but the main libraries implement all confidence bounds estimation procedure for us.

The main estimation procedures are related to:

Estimation of confidence bounds for means;

Estimation of confidence bounds for variances;

Estimation of confidence bounds for proportions.

We will see how to compute these practically in the laboratory sessions.

Confidence Intervals for Means#

We can compute confidence intervals for the estimation of means with scipy. Let us see how to compute confidence intervals for the mean of height:

from scipy import stats

mean = data['height'].mean()

std = np.std(data['height'])

standard_error = std/np.sqrt(len(data))

confidence_level = 0.95

interval = stats.norm.interval(confidence_level, loc=mean, scale=standard_error)

print(f"Estimated mean: {mean:0.2f}")

print(f"Standard deviation of the sample: {std:0.2f}")

print(f"Standard error of the sample: {standard_error:0.2f}")

print(f"Confidence interval: [{interval[0]:0.2f}, {interval[1]:0.2f}]")

Estimated mean: 169.89

Standard deviation of the sample: 9.96

Standard error of the sample: 0.15

Confidence interval: [169.59, 170.19]

Let us set the confidence level to \(0.99\):

from scipy import stats

mean = data['height'].mean()

std = np.std(data['height'])

standard_error = std/np.sqrt(len(data))

confidence_level = 0.99

interval = stats.norm.interval(confidence_level, loc=mean, scale=standard_error)

print(f"Estimated mean: {mean:0.2f}")

print(f"Standard deviation of the sample: {std:0.2f}")

print(f"Standard error of the sample: {standard_error:0.2f}")

print(f"Confidence interval: [{interval[0]:0.2f}, {interval[1]:0.2f}]")

Estimated mean: 169.89

Standard deviation of the sample: 9.96

Standard error of the sample: 0.15

Confidence interval: [169.50, 170.29]

Confidence Intervals for Variances#

To compute confidence intervals for the estimation of variances, we have to use the \(\chi^2\) distribution:

import numpy as np

from scipy import stats

# Set the desired confidence level

confidence_level = 0.95 # Change this to the desired confidence level (e.g., 0.95 for 95% confidence)

# Calculate the confidence interval for the population variance

confidence_interval = stats.chi2.interval(confidence_level, df=len(data) - 1)

# Calculate the sample variance

sample_variance = np.var(data['height'], ddof=1) # ddof=1 for sample variance

# Calculate the lower and upper bounds of the confidence interval

variance_lower = (len(data) - 1) * sample_variance / confidence_interval[1]

variance_upper = (len(data) - 1) * sample_variance / confidence_interval[0]

print(f"Sample Variance: {sample_variance:.2f}")

print(f"Confidence Interval for Variance: ({variance_lower:.2f}, {variance_upper:.2f})")

Sample Variance: 99.13

Confidence Interval for Variance: (95.04, 103.49)

Confidence Intervals for Proportion#

Let us see how to compute confidence intervals for the proportion of females over males:

import statsmodels.api as sm

import numpy as np

females = data['sex'].value_counts()['F']

total = len(data)

# Set the desired confidence level

confidence_level = 0.95 # Change this to the desired confidence level (e.g., 0.95 for 95% confidence)

# Calculate the proportion (sample proportion)

proportion = females / total

# Compute the confidence interval for the proportion

conf_interval = sm.stats.proportion_confint(females, total, alpha=1 - confidence_level, method='normal')

print(f"Sample Proportion: {proportion:.2f}")

print(f"Confidence Interval for Proportion: ({conf_interval[0]:.2f}, {conf_interval[1]:.2f})")

Sample Proportion: 0.54

Confidence Interval for Proportion: (0.53, 0.56)

Bootstrapping: Inference Through Resampling#

So far, we’ve built confidence intervals using formulas that rely on the Central Limit Theorem and assumptions about the underlying distribution (e.g., normality). But what if our sample size is small, the distribution is clearly not normal, or we want to find a confidence interval for a statistic where no simple formula exists (like the median)?

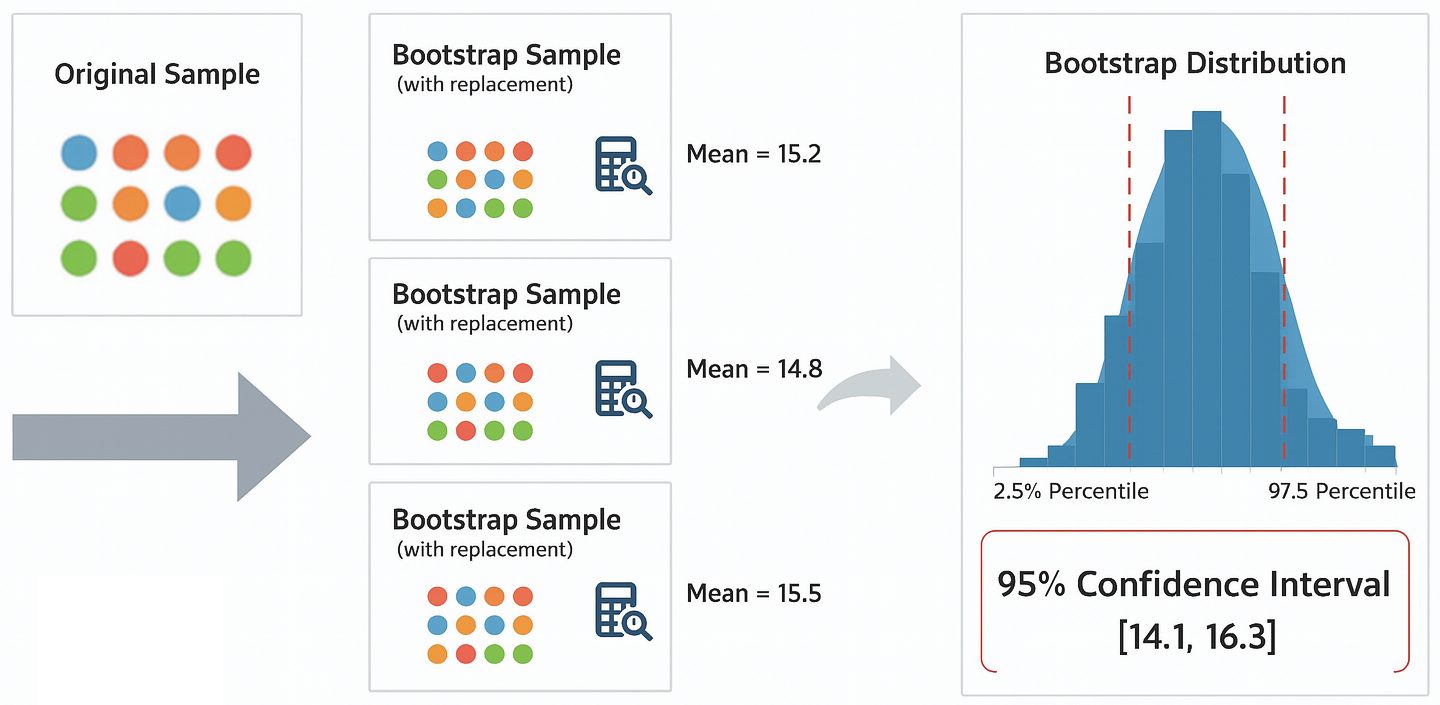

This is where bootstrapping comes in. It’s a powerful computational method that allows us to estimate the sampling distribution of any statistic using only our original sample. The name comes from the phrase “to pull oneself up by one’s own bootstraps”, reflecting the idea that we use the sample itself to learn about its own uncertainty.

The core idea is to treat the sample as a stand-in for the population. We then simulate the process of drawing new samples by resampling from our own sample.

The process is straightforward and relies on computation rather than complex formulas:

Start with your original sample of size \(n\).

Create a “bootstrap sample” by drawing \(n\) observations from your original sample with replacement. This new sample will be the same size as the original, but some data points may appear multiple times, while others may not appear at all.

Calculate the statistic of interest (e.g., mean, median, standard deviation) for this bootstrap sample.

Repeat steps 2 and 3 thousands of times (e.g., 10,000 times), recording the statistic each time.

Build the bootstrap distribution. The collection of all the statistics you calculated forms an empirical sampling distribution. We can now use this distribution to estimate properties like the standard error or confidence intervals.

For a 95% confidence interval, we can simply take the 2.5th and 97.5th percentiles of our bootstrap distribution.

Example: Bootstrap Confidence Interval for Mean Height#

Let’s use bootstrapping to find the 95% confidence interval for the mean height in our height_weight dataset.

import numpy as np

import pandas as pd

from scipy import stats

# Load the dataset

data = pd.read_csv('http://antoninofurnari.it/downloads/height_weight.csv')

original_sample = data['height']

# The data must be passed as a sequence (e.g., a tuple)

data_tuple = (original_sample,)

# Use scipy.stats.bootstrap to perform the resampling and calculate the interval

# We pass the data, the statistic to compute (np.mean), and the number of resamples.

bootstrap_result = stats.bootstrap(data_tuple, np.mean, n_resamples=10000, confidence_level=0.95)

# Extract the confidence interval from the result object

confidence_interval = bootstrap_result.confidence_interval

print(f"Original sample mean: {original_sample.mean():.2f}")

print(f"SciPy Bootstrap 95% Confidence Interval for the Mean: [{confidence_interval.low:.2f}, {confidence_interval.high:.2f}]")

Original sample mean: 169.89

SciPy Bootstrap 95% Confidence Interval for the Mean: [169.59, 170.19]

Bias and Variance of Estimators#

Let’s return to our bakery example. We want to estimate the true average weight \(\mu\) of cookie packages. To do this, we take a sample of \(n\) packages and compute the sample mean:

This formula is called an estimator of the population mean. The value we obtain from a specific sample is called an estimate. Since the sample changes each time we repeat the experiment, the estimate will vary.

It is useful to study how this estimator behaves across different samples—specifically, we want to understand its bias and variance.

Bias of an Estimator#

Let \(X\) be a random variable and let \(x = (x_1, x_2, \ldots, x_n)\) be a sample from the population. Let \(T(X)\) be an estimator of a population quantity \(\phi\) (for instance, the mean weight). Then:

is our estimator for \(\phi\). Since the sample changes, \(T(X)\) is a random variable.

The bias of the estimator is defined as:

This measures whether the estimator systematically overestimates or underestimates the true value. If:

then the estimator is unbiased, meaning that, on average, it gives the correct result.

In our case, the sample mean \(\overline{x}\) is an unbiased estimator of the population mean. If we repeated the sampling many times and averaged all the sample means, we would get a value close to \(\mu\).

Unbiased Estimator for the Variance#

To estimate the variance of cookie weights, we may compute:

This formula is biased—it tends to underestimate the true variance \(\sigma^2\). Specifically:

To correct this, we use the unbiased estimator:

This is the version we use when estimating the standard error and building confidence intervals. For large \(n\), the difference between \(s_n^2\) and \(s_{n-1}^2\) becomes negligible.

Variance of an Estimator#

The variance of an estimator tells us how much the estimate fluctuates across different samples. It is defined as:

A low variance means that repeated samples give similar results. A high variance means that estimates are unstable and vary widely.

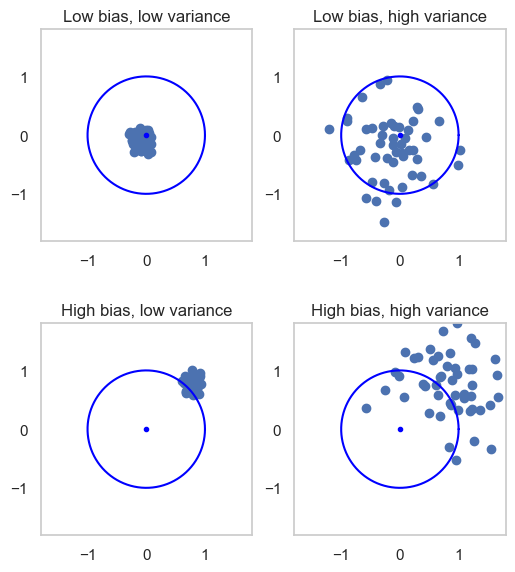

Bias-Variance Tradeoff#

Ideally, we want an estimator with low bias and low variance. This means that:

The estimates are close to each other (low variance),

And they are close to the true value (low bias).

In practice, we can visualize four scenarios:

Low bias, low variance: estimates are tightly clustered around the true value.

Low bias, high variance: estimates are scattered but centered correctly.

High bias, low variance: estimates are consistent but systematically wrong.

High bias, high variance: estimates are scattered and off-target.

This is often illustrated as a target with darts: the true value is the bullseye, and each dart is an estimate. The goal is to hit close to the center, consistently.

The four cases are:

Low bias, low variance: all estimates will be close to the true value;

Low bias, high variance: in average, estimates will be close to the true value, but different estimates may greatly differ;

High bias, low variance: while different estimates will be similar, they all are very far away from the true value;

High bias, high variance: we don’t have many guarantees - estimates will all be different, but also far from the real value, even in average.

It’s clear that having low bias and low variance is desirable, but, as we will see, this is not always easy to achieve. In practice, we’ll see that in many cases it there is a trade-off between bias and variance, meaning that we can tweak our estimator to find a balance between these two properties.

Hypothesis Testing#

Confidence intervals provide a range of plausible values for a population parameter based on a sample. A hypothesis test, instead, is used to challenge a specific claim about that parameter. Examples of hypotheses we might want to test include:

The average weight of cookie packages is exactly 1000g.

Two different ovens produce cookies with the same average weight.

The proportion of underweight packages is below a regulatory threshold.

If the hypothesis is rejected, we conclude that the claim is likely false. Otherwise, we do not have enough evidence to reject it, and we act as if it were true.

Hypothesis Testing for Cookie Weights#

Let’s return to our bakery. The packaging machine is set to produce cookie packages weighing exactly 1000g. We take a sample of \(n = 1000\) packages and compute:

We assume the small deviation is due to measurement noise or natural variation, and we are inclined to believe that the true mean is still \(\mu = 1000\)g.

However, our quality control manager raises a concern: what if the population mean is not 1000g? She proposes a formal test to challenge the assumption. We define:

Null hypothesis (\(H_0\)): the population mean is \(\mu_0 = 1000\)g

Alternative hypothesis (\(H_a\)): the population mean is different from 1000g

The null hypothesis is the hypothesis we are trying to reject (what we are trying to prove). If we do so, then we embrace the alternative hypothesis.

Before proceeding, we ask what margin of error is acceptable. The manager says she can tolerate a 5% chance of wrongly rejecting \(H_0\). This defines our significance level:

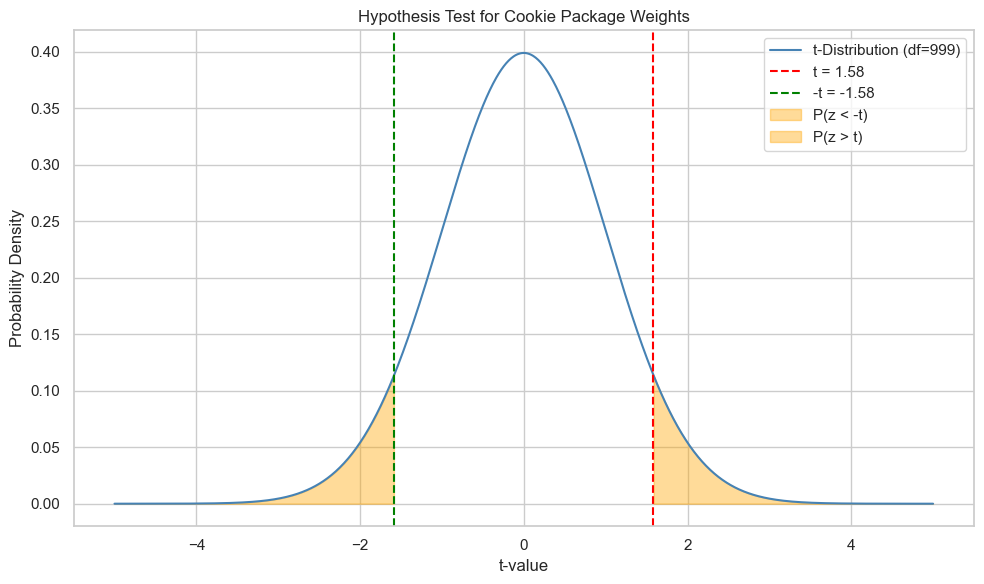

We now ask: how much does our sample mean \(\overline{x} = 1000.1g\) deviate from the assumed mean \(\mu_0 = 1000g\)? More precisely, what is the probability of observing a difference this large (or larger) just by chance?

To answer this, we compute the test statistic using the t-distribution:

This tells us how many standard errors our estimate is away from the hypothesized mean.

We now ask: what is the probability of observing a value this extreme or more extreme, assuming \(H_0\) is true? This is the p-value, defined as:

This is the area under the tails of the t-distribution beyond \(t\) and \(-t\):

Test statistic (t): 1.5811

Since the t-Student distribution is symmetrical, we can easily compute the p-value as:

In our case, we obtain:

t_stat = (x_bar - mu_0) / (s / np.sqrt(n))

print(f"{2*(1-t.cdf(t_stat, df, loc=0, scale=1)):0.2f}")

0.11

This is a large number! How to interpret it?

If the true mean is \(\mu=1000\) and we repeat sampling many times (\(n=1000\)), then \(11\%\) of the times we obtain a deviation more extreme than the observed one.

We now compare this number to the significance level of \(5\%\). If we reject the null hypothesis, we risk to make a mistake \(11\%\) of times (i.e., if we reject with this deviation, we should also reject for the other \(11\%\) of the times that the deviation is larger and we know that \(H_0\) is true), which is above the threshold of \(5\%\). Hence, we cannot reject the null hypothesis under these circumstances.

Does this mean that the two means are the same? We don’t know, the test does not tell us what to do in this case! But we may try to collect more measurements hoping to reduce uncertainty.

We suspect that our sample is too small, so we collect a total of \(n=5000\) examples and obtains:

The mean has decreased a little and the standard deviation has decreased. We recompute the statistic and obtain:

2.28

We have a larger (more extreme) statistic. We hence compute our p-value:

0.02

This p-value is now below the threshold of \(5\%\). We can now reject the null hypothesis and conclude that the population mean is different than \(1000g\).

Types of Errors in Statistical Tests#

Our statistical test provides evidence to either reject the null hypothesis in favor of the alternative or fail to reject it. However, since our decision is based on a sample, not the entire population, we can never be 100% certain. This uncertainty leads to the possibility of making two types of errors.

Type I Error (False Positive)#

A Type I Error occurs when we incorrectly reject a true null hypothesis. In other words, we conclude there is an effect or a difference when, in reality, there isn’t one.

The probability of committing a Type I error the significance level alpha (\(\alpha\)). When we set a significance level of \(\alpha = 0.05\), we are accepting a 5% risk of making a Type I error.

Type II Error (False Negative)#

A Type II Error occurs when we fail to reject a false null hypothesis. This means we miss a real effect or difference that actually exists.

Summary of Decisions#

We can summarize the relationship between our decision and reality in a table:

Null Hypothesis (\(H_0\)) is True |

Null Hypothesis (\(H_0\)) is False |

|

|---|---|---|

Fail to Reject \(H_0\) |

✅ Correct Decision (True Negative) |

❌ Type II Error (False Negative) |

Reject \(H_0\) |

❌ Type I Error (False Positive) |

✅ Correct Decision (True Positive) |

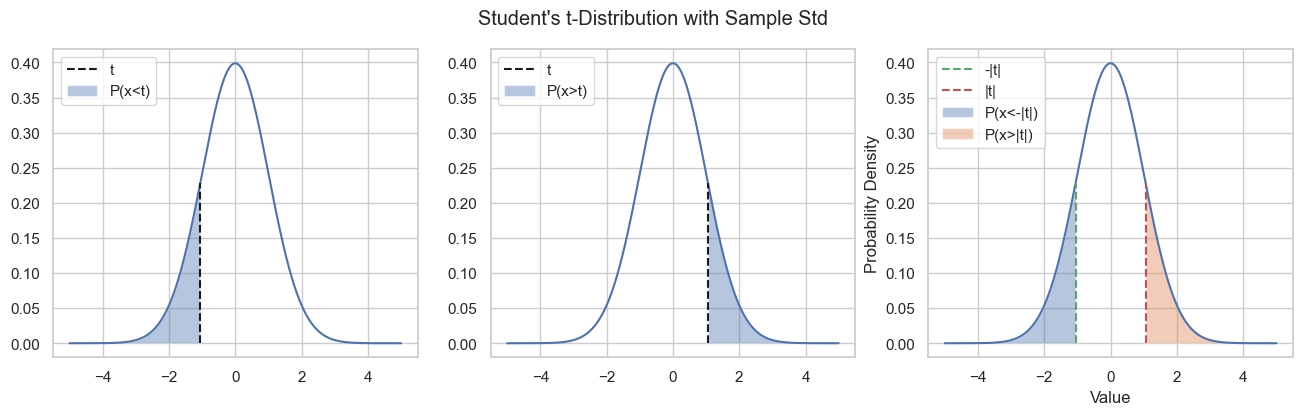

One-tailed vs Tow-tailed Tests#

The tests seen above is a “two-tailed test” in which we summed the areas in the two tails of the distribution. Depending on the form of the alternative hypothesis, in particular:

If the alternative hypothesis has the form \(\mu \neq \mu_0\), then we want to check when the deviation from the assumed mean is larger than the observed one: \(P(|x| > |z|)\);

If the alternative hypothesis has the form \(\mu > \mu_0\), then we want to check when the deviation from the assumed mean is positive and larger than the observed one: \(P(x > z)\);

If the alternative hypothesis has the form \(\mu < \mu_0\), then we want to check when the deviation from the assumed mean is negative and smaller than the observed one: \(P(x < z)\).

This will affect the computation of the p-value as shown in the following figure:

Hypotheses Tests in General#

A hypothesis test generally includes:

\(H_0\): the null hypothesis, e.g., the means of two populations are equal;

\(H_a\): the alternative hypothesis, e.g., the means of two populations are not equal (this determines if the test is one- or two-tailed);

a test statistics which quantifies how likely it is to reject the null hypothesis. The test statistics follows a specific distribution which depends on the type of statistical tests we are performing. E.g., it can follow a t-Student distribution;

a significance level \(\alpha\) which defines the sensitivity of the test. A common value is \(\alpha=0.05\), which means that we can wrongly reject the null hypothesis \(5\%\) of the times when it is in fact true. It represents the degree of error that we are willing to accept when performing hypothesis testing. Common values are \(0.1\), \(0.05\), \(0.01\);

the p-value: this quantifies the probability of sampling a test statistics at least as extreme as the one observed under the null hypothesis. In practice, the p-value measures the probability that the null hypothesis is true but we are observing test statistic leading to rejection nevertheless.

The null hypothesis is rejected if the p-value is larger than the chosen significance level \(\alpha\). We will not see in details all the possible hypothesis tests, but all of them follow a similar scheme.

Other Important Tests#

In this section, we briefly see the main statistical tests which can be used in practice, besides the one for means. We will not see how they are formulated, but we will see how to interpret them. We will see a few other tests when we’ll talk about linear regression.

One Sample T-Test#

This is the test for sample means we have previously seen. It is used to determine whether the mean of a single sample is significantly different from a known or hypothesized value.

This test allows to assess whether a sample has a given mean. Let us check if the average height in our dataset is equal to \(170cm\):

import numpy as np

from scipy import stats

# Define the null hypothesis mean (population mean you want to test against)

null_hypothesis_mean = 170

# Perform a one-sample t-test

t_stat, p_value = stats.ttest_1samp(data['height'], null_hypothesis_mean)

# Set the desired significance level (alpha)

alpha = 0.05

# Check the p-value against the significance level

if p_value < alpha:

print(f"Reject the null hypothesis. The data provides enough evidence to conclude that the population mean is different from {null_hypothesis_mean}.")

else:

print(f"Fail to reject the null hypothesis. The data does not provide enough evidence to conclude that the population mean is different from {null_hypothesis_mean}.")

print(f"t-statistic: {t_stat:.2f}")

print(f"P-value: {p_value:.4f}")

Fail to reject the null hypothesis. The data does not provide enough evidence to conclude that the population mean is different from 170.

t-statistic: -0.69

P-value: 0.4872

Let us now check if the average height is \(170\) among males only:

import numpy as np

from scipy import stats

# Define the null hypothesis mean (population mean you want to test against)

null_hypothesis_mean = 170

data2 = data[data['sex']=='M']

# Perform a one-sample t-test

t_stat, p_value = stats.ttest_1samp(data2['height'], null_hypothesis_mean)

# Set the desired significance level (alpha)

alpha = 0.05

# Check the p-value against the significance level

if p_value < alpha:

print(f"Reject the null hypothesis. The data provides enough evidence to conclude that the population mean is different from {null_hypothesis_mean}.")

else:

print(f"Fail to reject the null hypothesis. The data does not provide enough evidence to conclude that the population mean is different from {null_hypothesis_mean}.")

print(f"t-statistic: {t_stat:.2f}")

print(f"P-value: {p_value:.4f}")

Reject the null hypothesis. The data provides enough evidence to conclude that the population mean is different from 170.

t-statistic: 45.52

P-value: 0.0000

Two Sample T-Test#

A two-sample t-test is used to determine if there is a significant difference between the means of two independent samples. It’s often used when you want to compare the means of two different populations or treatments. The test assesses whether the difference between the sample means is statistically significant or if it could have occurred due to random chance. Also in this case, the test statistic will follow a t-Student distribution.

Let us now compare the average heights in two samples we previously obtained via random sampling. We expect no differences:

import scipy.stats as stats

h1 = sample1['height']

h2 = sample2['height']

# Perform independent two-sample t-test

t_stat, p_value = stats.ttest_ind(h1, h2)

# Define significance level (alpha)

alpha = 0.05

print(f"Test statistic: {t_stat:0.2f}")

print(f"Significance level: {alpha:0.2f}")

print(f"P-value: {p_value:0.2f}")

# Comment on result

if p_value < alpha:

print("Conclusion: there is a significant difference between the mean exam scores of the two classes.")

else:

print("Conclusion: there is no significant difference between the mean exam scores of the two classes.")

Test statistic: -0.47

Significance level: 0.05

P-value: 0.64

Conclusion: there is no significant difference between the mean exam scores of the two classes.

import pandas as pd

hw=pd.read_csv('http://antoninofurnari.it/downloads/height_weight.csv')

hw['height'] = (hw['height']/2.54).astype(int)

hw['weight'] = hw['weight']/2.205

hw

| sex | BMI | height | weight | |

|---|---|---|---|---|

| 0 | M | 33.36 | 74 | 53.484771 |

| 1 | M | 26.54 | 70 | 38.056472 |

| 2 | F | 32.13 | 61 | 34.970812 |

| 3 | M | 26.62 | 68 | 35.999365 |

| 4 | F | 27.13 | 66 | 34.559390 |

| ... | ... | ... | ... | ... |

| 4226 | F | 17.12 | 69 | 23.862436 |

| 4227 | M | 27.47 | 69 | 38.262182 |

| 4228 | F | 29.16 | 64 | 34.970812 |

| 4229 | F | 23.68 | 64 | 28.388071 |

| 4230 | F | 20.12 | 61 | 22.628172 |

4231 rows × 4 columns

If we compute the average BMI for males and females we obtain:

hw.groupby('sex')['BMI'].mean()

sex

F 26.929287

M 27.684959

Name: BMI, dtype: float64

We see a small difference. Is this due to chance or is it significant? If we run a two-sample t-test, we obtain the following results:

import scipy.stats as stats

male_bmi = hw[hw['sex']=='M']['BMI']

female_bmi = hw[hw['sex']=='F']['BMI']

# Perform independent two-sample t-test

t_stat, p_value = stats.ttest_ind(male_bmi, female_bmi)

# Define significance level (alpha)

alpha = 0.05

print(f"Test statistic: {t_stat:0.2f}")

print(f"Significance level: {alpha:0.2f}")

print(f"P-value: {p_value:0.2f}")

# Comment on result

if p_value < alpha:

print("Conclusion: there is a significant difference between the two means.")

else:

print("Conclusion: there is no significant difference between the two means.")

Test statistic: 4.64

Significance level: 0.05

P-value: 0.00

Conclusion: there is a significant difference between the two means.

Chi-Square Test for Independence#

The Chi-Square Test for Independence is a statistical test used to determine whether there is an association or independence between two or more categorical variables. This test is particularly useful when we want to assess whether changes in one categorical variable are related to changes in another categorical variable. The typical scenario is to set up a contingency table to compare the observed frequencies (counts) of the joint categories of the two variables to the expected frequencies that would occur under the assumption of independence.

The null hypothesis for the Chi-Square Test for Independence is that there is no association between the two categorical variables (they are independent), while the alternative hypothesis suggests that there is an association (they are dependent).

The test statistics follows a Chi-square distribution (we won’t see the details) in this case.

Let’s consider the Titanic dataset:

import pandas as pd

titanic = pd.read_csv('https://raw.githubusercontent.com/agconti/kaggle-titanic/master/data/train.csv',

index_col='PassengerId')

titanic

| Survived | Pclass | Name | Sex | Age | SibSp | Parch | Ticket | Fare | Cabin | Embarked | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| PassengerId | |||||||||||

| 1 | 0 | 3 | Braund, Mr. Owen Harris | male | 22.0 | 1 | 0 | A/5 21171 | 7.2500 | NaN | S |

| 2 | 1 | 1 | Cumings, Mrs. John Bradley (Florence Briggs Th... | female | 38.0 | 1 | 0 | PC 17599 | 71.2833 | C85 | C |

| 3 | 1 | 3 | Heikkinen, Miss. Laina | female | 26.0 | 0 | 0 | STON/O2. 3101282 | 7.9250 | NaN | S |

| 4 | 1 | 1 | Futrelle, Mrs. Jacques Heath (Lily May Peel) | female | 35.0 | 1 | 0 | 113803 | 53.1000 | C123 | S |

| 5 | 0 | 3 | Allen, Mr. William Henry | male | 35.0 | 0 | 0 | 373450 | 8.0500 | NaN | S |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 887 | 0 | 2 | Montvila, Rev. Juozas | male | 27.0 | 0 | 0 | 211536 | 13.0000 | NaN | S |

| 888 | 1 | 1 | Graham, Miss. Margaret Edith | female | 19.0 | 0 | 0 | 112053 | 30.0000 | B42 | S |

| 889 | 0 | 3 | Johnston, Miss. Catherine Helen "Carrie" | female | NaN | 1 | 2 | W./C. 6607 | 23.4500 | NaN | S |

| 890 | 1 | 1 | Behr, Mr. Karl Howell | male | 26.0 | 0 | 0 | 111369 | 30.0000 | C148 | C |

| 891 | 0 | 3 | Dooley, Mr. Patrick | male | 32.0 | 0 | 0 | 370376 | 7.7500 | NaN | Q |

891 rows × 11 columns

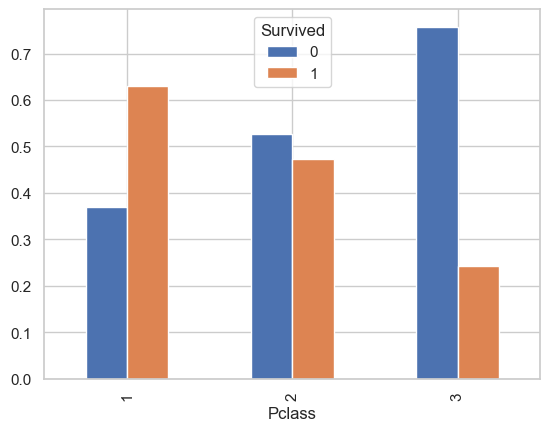

Let’s consider the following contingency table:

contingency_table = pd.crosstab(titanic['Pclass'], titanic['Survived'])

contingency_table

| Survived | 0 | 1 |

|---|---|---|

| Pclass | ||

| 1 | 80 | 136 |

| 2 | 97 | 87 |

| 3 | 372 | 119 |

We can visualize the distributions of Survived in the three classes for more clarity:

from matplotlib import pyplot as plt

pd.crosstab(titanic['Pclass'], titanic['Survived'], normalize=0).plot.bar()

plt.show()

We expect some form of correlation between the two variables. Indeed, the chi-square statistics and Cramer V statistics are:

from scipy.stats import chi2_contingency

from scipy.stats.contingency import association

print(f"Chi-square statistic: {chi2_contingency(contingency_table).statistic:0.2f}")

print(f"Cramer V statistic: {association(contingency_table):0.2f}")

Chi-square statistic: 102.89

Cramer V statistic: 0.34

We have numbers different from zero, but is this due to chance or is it statistically significant? If we run a chi-square contingency test:

import seaborn as sns

import pandas as pd

from scipy.stats import chi2_contingency

# Perform the Chi-Square Test for Independence

chi2, p, _, _ = chi2_contingency(contingency_table)

# Set the significance level (alpha)

alpha = 0.05

# Print the results

print("Chi-Square Statistic:", chi2)

print("p-value:", p)

# Interpret the results

if p < alpha:

print("\nThere is a significant association between 'Pclass' and 'survived'.")

else:

print("\nThere is no significant association between 'Pclass' and 'survived'.")

Chi-Square Statistic: 102.88898875696056

p-value: 4.549251711298793e-23

There is a significant association between 'Pclass' and 'survived'.

Chi-Square Goodness-of-Fit Test#

The Chi-Square Goodness of Fit test is a statistical test used to determine whether observed categorical data (frequencies) fit a specified distribution or expected frequencies. This test is often used to assess whether the observed data deviates significantly from a hypothesized distribution. The typical scenario is to compare observed frequencies with expected frequencies based on a theoretical model or prior knowledge.

The null hypothesis for the Chi-Square Goodness of Fit test is that there is no significant difference between the observed and expected frequencies, meaning the observed data fits the specified distribution. The alternative hypothesis suggests that there is a significant difference.

The test statistics follows a Chi-square distribution in this case.

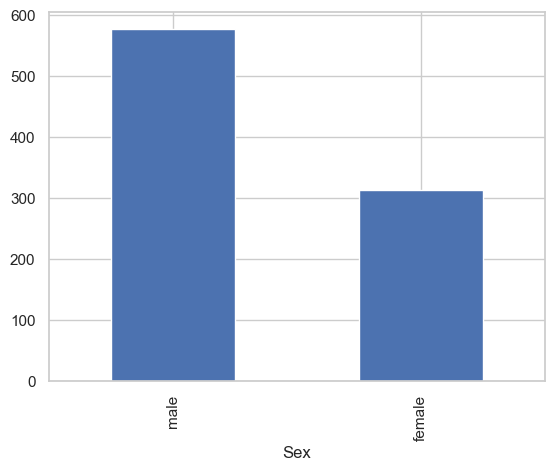

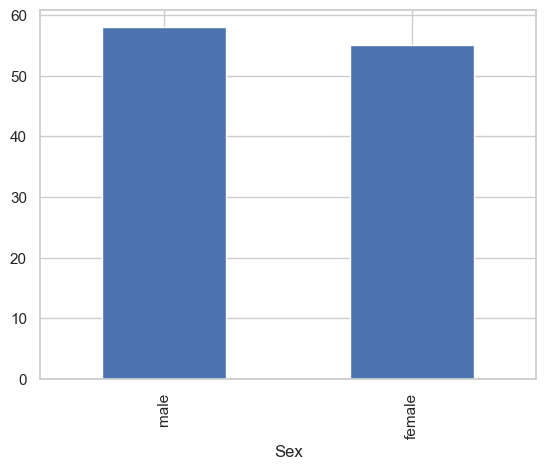

Let us consider the Titanic dataset again. We know that the distribution of Sex among passengers is biased:

titanic['Sex'].value_counts().plot.bar()

plt.show()

We now consider the distribution of Sex among passengers less than \(18\) years old:

minor=titanic[titanic['Age']<18]

observed_frequencies = minor['Sex'].value_counts()

observed_frequencies.plot.bar()

plt.show()

observed_frequencies

Sex

male 58

female 55

Name: count, dtype: int64

This looks less biased, but there are still minor differences between the counts. Are these due to chance? If Sex was distributed uniformly (as we hypothesize), we would have the following frequencies:

expected_frequencies = [113/2, 113/2]

expected_frequencies

[56.5, 56.5]

We can run a Goodness-of-fit test to check if the observed frequencies match the expected ones:

import seaborn as sns

import pandas as pd

from scipy.stats import chisquare

# Load the Titanic dataset

titanic_data = sns.load_dataset("titanic")

observed_frequencies = minor['Sex'].value_counts().values

# Define expected frequencies that closely match the observed data

expected_frequencies = [113/2, 113/2]

chi2, p_value = chisquare(f_obs=observed_frequencies, f_exp=expected_frequencies)

# Set the significance level (alpha)

alpha = 0.05

# Print the results

print("Observed Frequencies:")

print(observed_frequencies)

print("\nExpected Frequencies:")

print(expected_frequencies)

print("\nChi-Square Statistic:", chi2)

print("p-value:", p_value)

# Interpret the results

if p_value < alpha:

print("\nThe observed data significantly deviates from the expected distribution.")

else:

print("\nThe observed data fits the expected distribution.")

Observed Frequencies:

[58 55]

Expected Frequencies:

[56.5, 56.5]

Chi-Square Statistic: 0.07964601769911504

p-value: 0.7777776907897473

The observed data fits the expected distribution.

Given the large p-value, we could not reject the null hypothesis that there are significant differences between expected and observed frequencies.

Pearson/Spearman Correlation Test#

We have seen how to compute Pearson/Spearman correlation coefficient. However, what can we say when we get small values? Are those supposed to be zero, but we got something different from zero due to sampling, or are they significantly different from zero?

The statistical tests associated with the correlation coefficients are used to determine whether the observed correlation between two variables is statistically significant or if it might have occurred due to random chance. This test assesses whether the correlation in the sample data is likely to reflect a true correlation in the population.

The null hypothesis is that there is no statistically significant correlation between the two variables in the population. In other words, the true correlation coefficient in the population is zero.

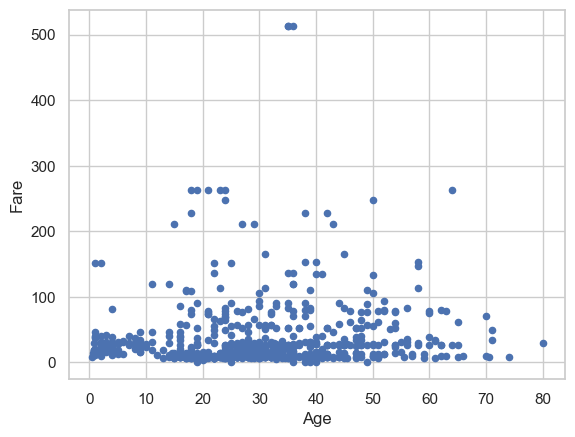

Let us consider the Titanic dataset. We find the following correlation between the Age and Fare variables:

titanic.plot.scatter(x='Age',y='Fare')

tt=titanic.dropna()

print(f"Correlation between age and fare: {titanic[['Age','Fare']].dropna().corr().values[0][1]:.2f}")

Correlation between age and fare: 0.10

Is this small positive correlation “true” or due to chance? Let us run a statistical test:

import seaborn as sns

import pandas as pd

import scipy.stats as stats

tt = titanic[['Age','Fare']].dropna()

# Extract the 'age' and 'fare' columns

age = tt['Age']

fare = tt['Fare']

# Perform a Pearson correlation test

r, p_value = stats.pearsonr(age, fare)

# Define the significance level

alpha = 0.05

# Display the results

print(f"Pearson correlation coefficient (r): {r}")

print(f"P-value: {p_value}")

# Compare the p-value to alpha

if p_value <= alpha:

print("Reject the null hypothesis. There is a significant correlation between age and fare.")

else:

print("Fail to reject the null hypothesis. There is no significant correlation between age and fare.")

Pearson correlation coefficient (r): 0.0960666917690389

P-value: 0.010216277504447016

Reject the null hypothesis. There is a significant correlation between age and fare.

The p-value is small enough to reject the null hypothesis: the correlation is small but statistically significant.

Similar tests exist for Spearman coefficient:

import seaborn as sns

import pandas as pd

import scipy.stats as stats

tt = titanic[['Age','Fare']].dropna()

# Extract the 'age' and 'fare' columns

age = tt['Age']

fare = tt['Fare']

# Perform a Pearson correlation test

r, p_value = stats.spearmanr(age, fare)

# Define the significance level

alpha = 0.05

# Display the results

print(f"Spearman correlation coefficient (r): {r}")

print(f"P-value: {p_value}")

# Compare the p-value to alpha

if p_value <= alpha:

print("Reject the null hypothesis. There is a significant correlation between age and fare.")

else:

print("Fail to reject the null hypothesis. There is no significant correlation between age and fare.")

Spearman correlation coefficient (r): 0.1350512177342878

P-value: 0.0002958090324306092

Reject the null hypothesis. There is a significant correlation between age and fare.

Assessing whether a Sample is Normally Distributed#

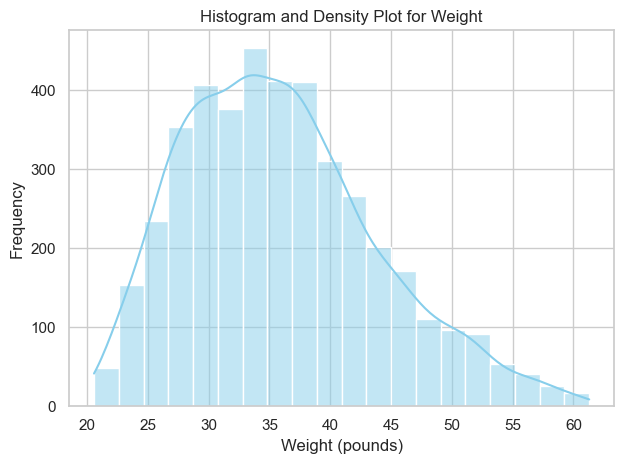

While the Normal distribution is pervasive, in some cases, it is useful to assess whether a given sample follows a normal distribution before assuming this is true. Let us consider the dataset of heights and weights and plot the distribution of weights:

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as plt

# Load the dataset

hw = pd.read_csv('http://antoninofurnari.it/downloads/height_weight.csv')

hw['height'] = (hw['height'] / 2.54).astype(int) # Convert height to inches

hw['weight'] = hw['weight'] / 2.205 # Convert weight to pounds

# Set up the plotting style

sns.set(style="whitegrid")

# Plotting for weight

sns.histplot(hw['weight'], kde=True, color="skyblue", bins=20)

plt.title('Histogram and Density Plot for Weight')

plt.xlabel('Weight (pounds)')

plt.ylabel('Frequency')

plt.tight_layout()

plt.show()

Does the distribution look Gaussian? Let us compute Skewness and Kurtosis:

import pandas as pd

from scipy.stats import skew, kurtosis

# Load and preprocess the data

hw = pd.read_csv('http://antoninofurnari.it/downloads/height_weight_pounds.csv')

# Calculate skewness and kurtosis for weight

weight_skewness = skew(hw['weight'])

weight_kurtosis = kurtosis(hw['weight'])

print(f"Skewness of weight: {weight_skewness:.2f}")

print(f"Kurtosis of weight: {weight_kurtosis:.2f}")

Skewness of weight: 0.57

Kurtosis of weight: -0.06

We not that:

We have a positive Skewness: this indicates that the distribution is skewed towards the right side (the right tail is longer) as compared to a Normal distribution;

We have a Kurtosis slightly lower than zero: the distribution is slightly “flatter” than a Normal distribution.

While Skewness and Kurtosis can help characterize deviations from normality, there are tests which can be used.

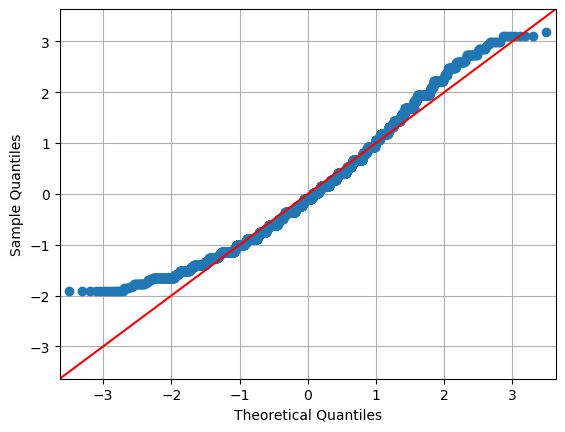

Quantile-Quantile Plots (Q-Q Plots)#

Quantile-Quantile plots, or Q-Q plots, are a powerful tool to assess how well a sample matches a theoretical distribution. The idea is simple: we compare the quantiles of the empirical data with the quantiles of a reference distribution—typically the normal distribution.

To make the comparison meaningful and remove scale effects, the empirical data is often standardized into z-scores. If the sample truly follows the theoretical distribution, the quantiles will align, and the points will fall along the diagonal line \(y = x\).

Deviations from this line reveal systematic differences between the empirical and theoretical distributions. For example:

A curve that bends away from the diagonal suggests skewness.

S-shaped patterns may indicate heavier or lighter tails than expected.

In the following graph, we show the Q-Q plot for the sample of cookie package weights. It helps us visually evaluate whether the sample distribution is approximately normal—a key assumption in many statistical methods.

from statsmodels.graphics.gofplots import qqplot

import pandas as pd

from matplotlib import pyplot as plt

# fit=True means the distribution should be fitted to the data

# and the data should be standardized

# line='45' means a 45-degree reference line will be plotted

qqplot(hw['weight'], fit=True, line='45')

plt.grid()

plt.show()

The plot relates the “theoretical” quantiles with those of the sample. The fact that the points on the plot do not lie on the diagonal indicates that there is a discrepancy between the empirical data distribution and the Gaussian distribution.

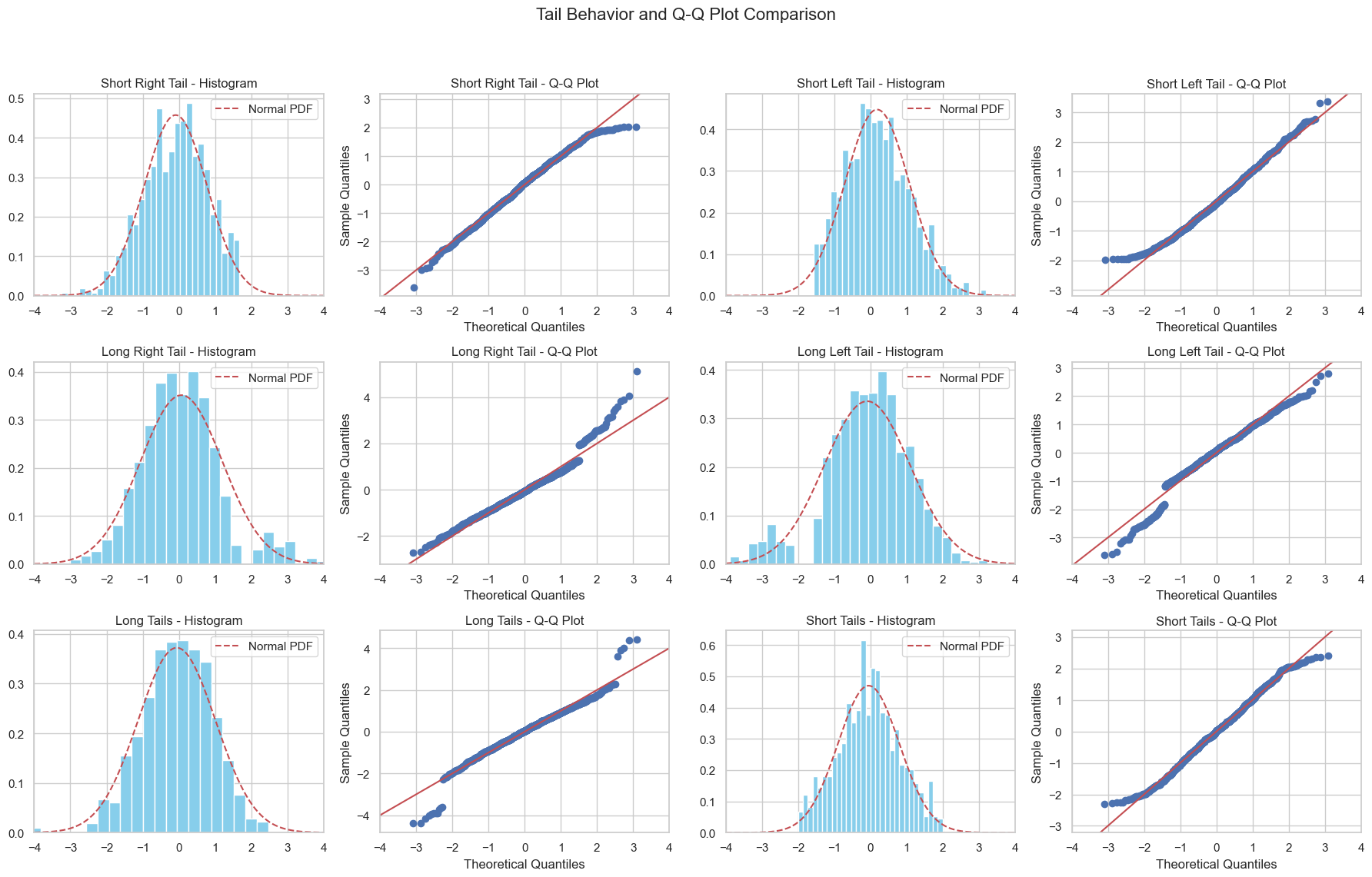

Analyzing a Q-Q Plot can be complex. In practice, there are some guidelines to understand how a sample deviates from a theoretical distribution. The following figure compares the q-q plots of different distributions:

Every time we observe a Q-Q Plot, we can relate these features to characteristics of the distribution. Clearly, these characteristics can also combine to create more complex Q-Q Plots, as seen in the case of weights.

Shapiro-Wilk Normality Test#

The Shapiro-Wilk test is a statistical test used to assess whether a sample follows a Gaussian (normal) distribution. It is used with small samples (\(n\leq 2000\)) It works by comparing the observed data to what you would expect if the data were drawn from a truly Gaussian distribution.

The null hypothesis for this test is that the population is normally distributed.

We will not see the formal details of this test, but we can use it in our analyses. Here is the result on the weight sample in our height-weight dataset:

from scipy.stats import shapiro

import pandas as pd

# Perform the Shapiro-Wilk test

statistic, p_value = shapiro(hw['weight'])

# Set the significance level (alpha)

alpha = 0.05

print(f"Test statistic: {statistic:0.2f}")

print(f"P-value: {p_value:0.2f}")

# Check the p-value against the significance level

if p_value > alpha:

print("Sample looks Gaussian (fail to reject H0)")

else:

print("Sample does not look Gaussian (reject H0)")

Test statistic: 0.97

P-value: 0.00

Sample does not look Gaussian (reject H0)

D’Agostino’s K-squared test#

When samples are large (\(n \geq 50\)), the D’Agostino’s K-squared test is more used. It is based on Skewness and Kurtosis.

The null hypothesis for this test is that the population is normally distributed.

Here is the result for our example:

import pandas as pd

from scipy.stats import normaltest

# Perform D'Agostino's K-squared test

statistic, p_value = normaltest(hw['weight'])

# Set the significance level (alpha)

alpha = 0.05

print(f"Test statistic: {statistic:.2f}")

print(f"P-value: {p_value:.2f}")

# Check the p-value against the significance level

if p_value > alpha:

print("Sample looks Gaussian (fail to reject H0)")

else:

print("Sample does not look Gaussian (reject H0)")

Test statistic: 201.64

P-value: 0.00

Sample does not look Gaussian (reject H0)

Exercises#

Exercise 1

Consider the sample of all passengers in the titanic dataset. Compute the mean age of all passengers. Then, compute the confidence bounds for this mean setting the confidence level to 0.95. Is the estimated mean a reliable estimate of the population mean?

Exercise 2

Consider the samples of all passengers in the titanic dataset. Compute the variance of the ages of all passengers. Then, compute the confidence bounds for this variance setting the confidence level to 0.95. Is the estimated variance a reliable estimate of the population variance?

Exercise 3

Extract the sample of values of Sex of passengers in second class in the titanic dataset. Compute the contingency table of absolute counts of the Sex column. Compute the confidence bounds for the proportions of Sex in the sample. Are the estimated bounds reliable? Repeat the analysis for class 1 and 3.

Exercise 4

The average age of women in the US population is 40. Run a statistical test to assess whether the sample of ages in the

infertdataset has the same mean as the US population. What is the result of the test? Are women ininfertyounger or older than the average?You can load the dataset installing the

pydatasetlibrary withpip install pydatasetand then:

from pydataset import data; infert = data("infert")

Exercise 5

Consider the

titanicdataset. Follow these steps to assess that males and females are not equally distributed:

Obtain a table of absolute frequencies of the values of

Sex;Show a barplot comparing the proportions of male and female passengers. Do these look equally distributed?

Run a statistical test to assess whether the proportion of males and females are equal (\(p=0.5\)). What is the result of the test?

Run the statistical test setting \(p=1/3\). Is the result different? Can we reject the null hypothesis? Why?

References#

Chapters 6-8 of [1];

Parts of chapter 9 of [2].

[1] Gonick, L., & Smith, W. (1993). The cartoon guide to statistics. HarperCollins Publishers, Inc.

[2] Heumann, Christian, and Michael Schomaker Shalabh. Introduction to statistics and data analysis. Springer International Publishing Switzerland, 2016.